The global wind industry installed a record-breaking 165 GW of new wind capacity in 2025, up 40 per cent from 2024, according to the “2026 Global Wind Report,” newly released by the Global Wind Energy Council (GWEC).

Global wind capacity reached 1,299 GW by the end of 2025, with 138 countries now powering their economies with wind power.

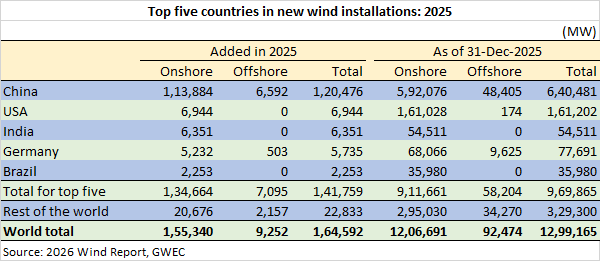

The report reveals that the two largest markets in Asia — China and India — together added more than 126 GW in 2025. China alone added more than 120 GW, while India almost doubled annual installations to build a record 6.3 GW of new capacity in 2025.

In the United States, annual onshore wind installations increased by almost 7 GW – demonstrating the strength of an industry underpinned by strong economic fundamentals.

Of the 165 GW installed in 2025, onshore installations accounted for 155.3 GW (up 42 per cent year-on-year) while 9.3 GW came from offshore farms (up 16 per cent).

A total of 57 countries contributed to new global wind power capacity coming online in 2025.

China once again led the way for new wind installations ahead of the USA, India, Germany, and Brazil. Combined, they made up 86 per cent of global additions in 2025. Those same five markets also made up the top five for global installed wind capacity, comprising 75 per cent of the world’s total.

China dominated new onshore wind installations in 2025, adding more than 110 GW, or 73 per cent of the global total. In addition, more than 124 GW of future capacity was approved in 2025 under the country’s new market-oriented pricing mechanism in 2025, a third higher than the previous year.

The USA commissioned the next highest volume of onshore wind, at nearly 7 GW, in 2025. This was up 71 per cent year-on-year, comprising a rebound for the country after four years of declining growth. India also saw its onshore wind market surge in 2025. The country added a record 6.3 GW of new capacity in 2025 (up 86 per cent) followed by Germany (5.2 GW) and Brazil (2.3 GW).

New onshore wind capacity awarded worldwide through wind-specific, technology-neutral, renewable and hybrid auctions was 32.8 GW, 39 per cent lower than 2024. More than half of this was in Europe and around one-third in the Asia-Pacific region, primarily in India.

Some 9.2 GW of new offshore wind capacity was grid connected worldwide in 2025, bringing the total installed to 92.3 GW and approaching an historic 100 GW milestone. China accounted for 6.6 GW of new offshore wind capacity, while Europe commissioned nearly 2 GW, with the UK connecting over 1 GW.

The path to 2 TW

In the next five years between 2026 and 2030, GWEC Market Intelligence projects a total of 969 GW of new wind capacity is expected to be commissioned, averaging 194 GW annually through 2030. This amounts to a projected compound annual average growth rate of 5.2 per cent.

While China is expected to drive an estimated 63 per cent of new installations in 2026, greater diversification in the market is expected by 2030. As a result of rapid acceleration in regions such as Southeast Asia, Central Asia and Africa & Middle East from 2027, more than half of global growth is expected to come from markets outside of China by the end of the decade.

Global wind capacity is now projected expected to surpass the historic 2-TW milestone by 2029 – just six years after crossing 1-TW in 2023.

Also read: Vestas retains global wind market leadership in 2020

Featured photograph (source: GWEC’s 2026 Global Wind Report) is for representation only