Let us start by understanding the rationale behind floating an investment trust as opposed to listing the main company (Sterlite Power Grid Ventures) itself?

India’s infrastructure sector requires $200 billion investment to achieve its growth vision. A substantial portion of this investment is envisaged via private sector participation. This would need harnessing investments from foreign institutions, domestic institutions as well as retail investors.

Sterlite Power is one of the largest private sector transmission companies that bids, develops and executes large power transmission projects. Considering the fact that development and ownership of transmission assets is a capital-intensive business, harnessing the above-mentioned capital sources is essential for investment in development of transmission assets.

Ownership of completed power transmission projects offers long-term stable yield with perpetual ownership of assets and predictable cash flows for at least 35 years. However, development of transmission assets is a considerably risky business on account of project execution risks, RoW issues and several clearances required across state and central agencies.

With the above two things in mind – capital intensive nature of power transmission business and substantial risk reduction post commissioning of project, we believed that a platform focused on operating transmission projects would provide a better investment opportunity for investors as well as lead to an optimum way to raise capital. This would also enable Sterlite power or even other developers to release equity capital by selling operating projects to IndiGrid and invest it in creating new assets.

Ownership of completed power transmission projects offers long-term stable yield with perpetual ownership of assets and predictable cash flows for at least 35 years.

Why do you believe that this model will work well? What is the global experience?

We believe this model works successfully because:

- It allows investors like (FIIs, banks, insurance companies, pension funds, retail investors) to invest well-governed yield-generating operating assets with predictable cash flows and low volatility.

- It enables developers to invest more in the development projects and create more capacity.

Globally this model has worked very well. Till date, there have been over 400 listings of similar instruments accounting for over $1 trillion of investments across the world. These instruments have assisted countries to meet their capital needs for the infrastructure and real estate sectors. Long-term infrastructure assets like roads, power generation, telecom towers, power transmission, warehouses, ports, gas pipelines etc. are owned by such platforms which offer investors stable income and growth for long-term. They are considered as high dividend-paying investments suitable for investors looking for long-term, stable cash flow with moderate capital appreciation.

IndiGrid is India’s first power-sector infrastructure InvIT. How has been the performance so far, in terms of returns to unitholders?

Since our listing in June 2017 with two transmission assets, we further acquired six more operational transmission assets over the last 18 months and expanded the portfolio size almost three times, from Rs.3,800 crore to Rs.11,100 crore. We have also secured an additional asset pipeline of Rs.7,500 crore which provides us strong visibility for future growth. Our quarterly distributions have grown from Rs.78 crore to Rs.175 crore.

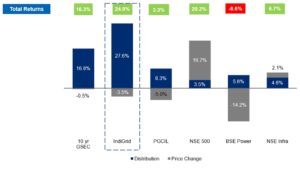

We listed in June 2017 with a focus on providing superior risk-adjusted return to investors and grow it consistently. We have delivered total return of 24 per cent since listing in June 2017. We have delivered Rs.27.6 distribution per unit to our investors. We have been a low volatility entity with a Beta of 0.07.

The following chart elaborates how IndiGrid has performed since listing in comparison to comparable equity indices, dividend paying stock in the same sector (power transmission), NSE 500 as well as the 10-year GSEC.

Source: Bloomberg

Note: Total Return chart and Beta calculations (weekly basis) are from IndiGrid’s listing date June 6, 2017 to November 29, 2019

What is the current portfolio of IndiGrid in terms of number of power transmission lines, length, transformation capacity, etc.?

IndiGrid currently owns eight operational power transmission assets consisting of 22 revenue generating elements—18 transmission lines of 4,900 ckm and 4 substations of 7,735 MVA transformation capacity across 11 states in India with residual contract life of ~32 years.

Our portfolio will further grow to 32 transmission lines of 6,600 ckm and 10 substations of 14,995 MVA capacity post acquisition of assets on which we have exclusive agreements.

IndiGrid currently owns eight operational power transmission assets with an AUM of around Rs.11,100 crore. It has a strong pipeline visibility by virtue of exclusive agreements to acquire another four projects which would increase the portfolio to Rs.18,000 crore over the next two years

Please tell us in brief about the various entities associated with IndiGrid, like the trustee, investment manager, etc.

InvITs are formed by complying with the SEBI Infrastructure Investment Trust Regulation, 2014. There are four important parties to any InvIT —Investment Manager, Sponsor, Project Manager and the Trustee.

The Investment manager is responsible for operations pertaining to the Trust, such as distribution of cash flows, acquisition/ divestment of assets etc. along with all decisions in relation to the management and administration of IndiGrid’s assets and the investments of IndiGrid. Sterlite Investment Managers Ltd is the investment manager for IndiGrid. KKR owns majority of the investment manager.

A Sponsor is the one who sets up the InvIT and appoints the trustee. The Sponsor has to hold a minimum of 15 per cent of total units in an InvIT for three years since listing as per regulations. Sterlite Power Grid Ventures Ltd is the sponsor of IndiGrid. KKR has also expressed interest in becoming the sponsor of IndiGrid, which has been approved by unit holders as well. However, this is subject to SEBI approval.

The Project Manager is appointed by the Investment Manager for operating and maintaining the assets. It is overseen by the investment manager and the trustee. Sterlite Power acts as the Project Manager for IndiGrid.

The Trustee, independent of the Sponsor and Investment Manager, is entrusted with the custody of the assets ensuring highest standards of corporate governance. who must ensure that the functions of the InvIT, Investment Manager and Project Manager comply with SEBI rules. Axis Trustee Services Ltd serves as the trustee for IndiGrid,

What is the size of the portfolio, in terms of assets under management (AUM)? Do you have any AUM target for the next 3-5 years, say?

IndiGrid currently owns eight operational power transmission assets with an AUM of around Rs.11,100 crore. It has a strong pipeline visibility by virtue of exclusive agreements to acquire another four projects which would increase the portfolio of Rs.18,000 crore over the next two years, which implies a five-fold growth since listing of the platform.

We remain driven by our vision to become the most admired yield vehicle in Asia and committed to our aim of achieving AUM of Rs.30,000 crore by 2022. Having said that, we are more focused on accretive acquisitions rather than just add to our AUM.

Apart from power transmission lines developed by Sterlite Power, we understand that you have also acquired assets owned by other developers. Tell us more.

Our focus is to acquire projects with long contract period and low operating risk which adds to the predictable yield for our investors. We remain committed to achieving accretive growth not only through the acquisition of its sponsor assets but through the acquisition of third-party assets. We keep evaluating many opportunities beyond the identified assets with Sterlite Power.

The current power transmission sector landscape is very robust across around 15,000 ckm and transformative capacity of some 17,000 MVA with a total of around 22 interstate and intrastate projects. We also see that over Rs.10,000 crore worth of bidding opportunities exist right now. This, for IndiGrid, provides a very good growth outlook going forward beyond 2022. Moreover, there is also the opportunity of public monetization by state and central transmission companies (transcos), should they choose to monetize.

In August 2018, IndiGrid acquired its first third-party transmission asset, Patran Transmission Company, a 1,000 MVA transmission asset located in Punjab, from Techno Electric & Engineering Company Ltd.

What is your resource-mobilization plan so as to finance new acquisitions?

Our business strategy is to acquire operating projects. This requires substantial resource mobilization as and when we acquire projects. IndiGrid is committed to maintain a maximum of 70 per cent consolidated debt to AUM ratio as per regulations prescribed by SEBI. This requires both equity and debt raising appropriately.

Our recent preferential issue of Rs.2,514 crore in May 2019 was highly successful with participation from marquee investors including KKR and GIC. KKR also expressed interest to become a sponsor of IndiGrid and acquired majority interest in the investment manager of IndiGrid. With this preferential issue, our net debt/AUM ratio is only 44 per cent. Therefore, there is enough headroom for us to acquire more projects without incremental capital raise.

With the backing of investors such as KKR and GIC who are keen to deploy more capital for the growth of this platform for value-accretive projects, we are confident that equity capital will be available for good projects. In addition, we are also working with SEBI to enable rights issue for InvITs which will enable all existing investors to participate equally in any new capital raises.

We have also raised Rs.5,500 crore debt from diverse set of investors including banks, mutual funds, ECB etc. We are rated AAA by several rating agencies, and we tap most efficient sources of debt capital with respect to tenure and cost.

The Green Energy Corridor (GEC) envisages 3,200 ckm of power transmission lines under the interstate transmission system. Would lines under the GEC would be of interest to IndiGrid?

While IndiGrid’s business strategy is to focus largely on acquiring operational assets, the GEC projects are another opportunity for us to buy a new project upon its COD (commercial operation date). The GEC projects awarded are under the TBCB mechanism and are part of inter-state transmission scheme (ISTS). Our entire portfolio is of the ISTS regime and we would certainly evaluate GEC lines as and when they are commissioned.

The passage of the Electricity Act, 2003 promoting competition represented a landmark moment for the Indian power sector, and its effective implementation has attracted and nurtured private participation.

There are emerging instances of interstate lines being developed on the TBCB modality. Would intrastate lines also be of interest to IndiGrid?

So far as you know all the eight projects and the four pipeline projects in the IndiGrid portfolio are part of ISTS which is paid out of the point of connection (PoC) pool. It is true that some states could be considered riskier than the interstate pool, so there are few specific points we need to consider for intrastate projects with respect to the payment security mechanism, strength of concession agreements etc.

However, we do not believe that the intrastate opportunity in terms of operating projects is as large as ISTS at the moment. However, in case there is an opportunity to acquire projects with strong contractual arrangement and payment security, we may consider it. Having said that, considering our greater focus on ISTS lines, such intrastate lines may remain a very small fraction of our portfolio, if at all an opportunity arises.

Do you feel that the TBCB philosophy in interstate power transmission has sufficiently progressed in India? How can the TBCB movement be propelled further?

The passage of the Electricity Act, 2003 promoting competition represented a landmark moment for the Indian power sector, and its effective implementation has attracted and nurtured private participation. The tariff-based competitive bidding (TBCB) mechanism opened development of transmission projects to private sector.

The private sector accounted for 41 per cent out of a total of Rs.1,03,000 crore invested on transmission asset creation since 2011. A very important enabler of private sector participation was the revenue security brought in by the Point of Connection (PoC) mechanism in the Inter-State Transmission Network (ISTN).

Project execution models based on competitive bidding have demonstrated the capability of developers to work strictly according to timelines under a transparent framework. Even public sector undertakings like Power Grid Corporation have bid substantial projects under TBCB and achieved improved efficiencies of cost and time in the projects secured through competitive bidding.

TBCB mechanism enables the much-required global investment in the power transmission sector and multiple companies to work on overall National Grid of India which results in swifter capacity augmentation and efficiencies in cost and time.

Owing to its initial success over last decade, the Ministry of Power should consider a large scale build-out of national grid on TBCB basis where all companies including PGCIL can bid and bring efficiency in terms of cost and speed of capacity enhancement that’s needed for the new energy mix.

It is also important that the bidding timeline of five months for TBCB projects be reduced to about 70 days (approximately 2.5 months) by following a single-stage process that is already being practiced for selection of RE developers by SECI and award transmission schemes faster through TBCB process.